The Southeast Asia foodservice market is expected to reach USD 465.45 billion by 2031 at 12.98% CAGR over 2026-2031. Western food brands failing at market entry is not a story about a small or speculative market. The capital flowing into Southeast Asia F&B from Western entrants is calibrated to a real growth signal.

The failure rate is equally real and consistent enough across Malaysia, Indonesia, Vietnam, Thailand, and the Philippines to warrant a structural explanation rather than a case-by-case post-mortem.

The conventional diagnosis is cultural misread: Western brands fail because they do not understand local taste preferences. That diagnosis is not wrong, but it is downstream of a more fundamental error. Three structural misreads account for most of the pattern.

The first is competitive: local brands did not catch up to Western entrants; in several markets, Western challengers had already won before they arrived with meaningful scale. The second is architectural: independent outlets hold 70% of the Southeast Asia foodservice market, a distribution environment that most Western market entry strategies are not built to reach.

The third is definitional: what Western brands call localisation is, in most documented cases, brand-level adaptation that leaves price architecture and distribution model unchanged.

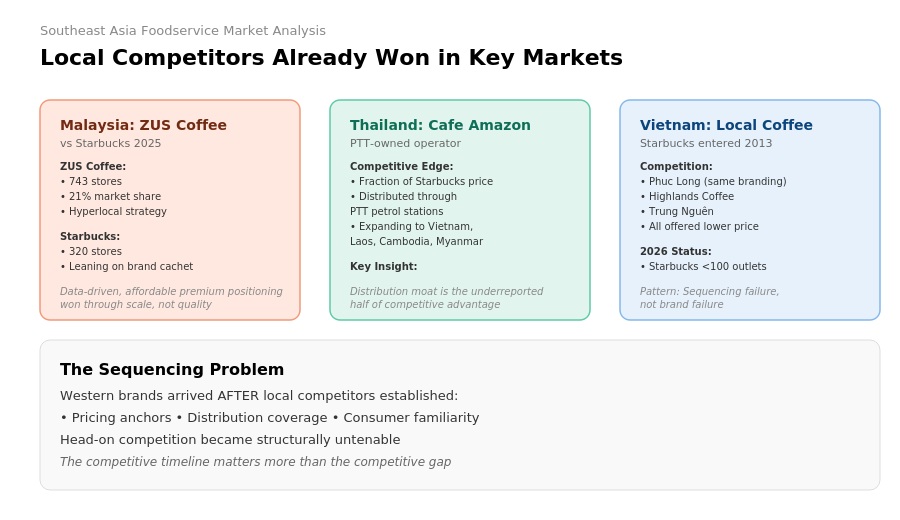

Argument 1: Local Competitors Are Not Catching Up — They Already Won in Malaysia, Thailand, and Vietnam

The competitive timeline matters more than the competitive gap. In Malaysia, Thailand, and Vietnam, the local winners were not start-ups scrambling to match Western standards; they were established operators with distribution coverage, consumer familiarity, and pricing infrastructure that Western entrants could not replicate on entry.

ZUS Coffee vs Starbucks in Malaysia 2025

By 2025, ZUS Coffee had surpassed Starbucks in Malaysia on store count: 743 stores to Starbucks’ 320, capturing 21% national market share. ZUS did not close that gap on product quality or brand equity. It did so through a data-driven hyperlocal strategy, an app-first loyalty model, and pricing that positioned it as affordable premium rather than aspirational Western.

Starbucks’ documented response was to lean further into global brand cachet: strategic local partnerships, limited-edition collaborations, and digital ordering enhancements. That response confirmed the direction of the competitive shift rather than reversed it.

“We have grown quite quickly across countries, not because we are the cheapest; often local competitors are cheaper than us. However, we have localised the offering and used technology to increase sales per store.” — Muhammad Chandra Liong, CEO, Kenangan Coffee

Tracking food industry trends in Asia through the lens of store-count data rather than brand health surveys gives a different picture of who is winning.

Cafe Amazon in Thailand

Cafe Amazon, owned by PTT, Thailand’s national oil company, operates outlets across Thailand and is expanding into Vietnam, Laos, Cambodia, and Myanmar. It prices at a fraction of Starbucks and distributes through PTT petrol stations: an infrastructure no Western F&B entrant has built or replicated.

Local players like Cafe Amazon and ZUS Coffee are entrenched in Malaysia and Thailand with significant store footprint and prices that are sometimes cheaper than Western brands.

Even those, like Luckin Coffee, that entered Singapore with aggressive low-price kiosk models. The distribution moat is the underreported half of the competitive advantage.

Phuc Long and Highlands Coffee in Vietnam

Starbucks entered Ho Chi Minh City in 2013. Phuc Long opened within metres, with similar visual branding, lower price, and Vietnamese origin. In a 2015 FT Confidential Research survey across 1,000 consumers each in the five largest ASEAN economies, Vietnam was the only market where Starbucks was not the most frequently visited chain; Trung Nguên and Highlands Coffee dominated.

By 2026, Starbucks Vietnam still operated fewer than 100 outlets nationally. The pattern across Malaysia, Thailand, and Vietnam is not brand failure; it is sequencing failure.

Western brands arrived after local competitors had established pricing anchors, distribution coverage, and consumer familiarity at a scale that made head-on competition structurally untenable.

Argument 2: The Market Structure Western Brands Are Entering Does Not Exist at the Scale They Assume

In 2024–2025, independent outlets held the majority of the Southeast Asia foodservice market, reflecting the region’s strong preference for authentic, locally-inspired food experiences

A Western brand that constructs its Southeast Asia entry around modern retail chains, premium shopping mall placements, and master franchise agreements is designing a strategy for 30% of the addressable market. The other 70% requires a distribution infrastructure that most Western entrants neither have nor build for.

This is not a condition of underdevelopment on the way to modernisation. In Indonesia, Southeast Asia’s largest foodservice market is exepected surpass USD 128 billion by 2031, and in Vietnam, the independent-outlet-dominant structure is the current operating reality, not a transitional phase.

Understanding what emerging food markets in Southeast Asia actually look like in distribution terms is the prerequisite the market sizing number does not supply.

Price Sensitivity in Indonesia and Vietnam F&B

In Indonesia, approximately IDR 1,000, roughly USD 0.06–0.10, is the minimum sustainable price floor for common household F&B items: the point below which consumers do not expect to pay for everyday products.

Western brands calibrating price points to Singapore or Kuala Lumpur premium retail are not competing in the same market as their prospective Indonesian consumers. Forty-two percent of Southeast Asian consumers now actively seek the same products at lower prices; one-quarter are switching brands for better value.

These are not post-inflation sentiment readings; they describe a structural feature of consumer food trends in Asia in the income segments that represent the majority of the region’s foodservice market.

Beyond Meat Asia failure: Plant-based Meets Structural Misread

The Beyond Meat Asia failure plant-based trajectory is now a documented case study in what structural misread produces at scale: a full-year operating loss of USD 332.7 million in 2025, more than double the USD 156.1 million loss in 2024, and exit from China by mid-2025.

The product did not fail on taste. It failed because Asian plant-based alternatives such as tofu, tempeh, fermented soy, and Buddhist protein traditions across Indonesia, Vietnam, and Thailand are already occupying the same consumer need at a price point Western-format products could not match.

The category existed before Beyond Meat arrived. Its Western format of that category did not fit the market structure it entered.

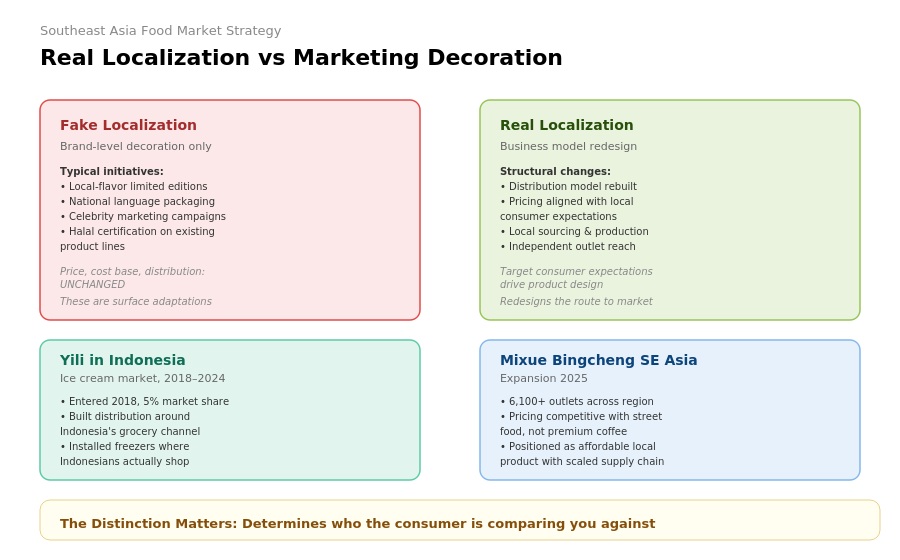

Argument 3: Localisation at the Brand Level Is Not Localisation — It Is Decoration

Western brands that document their Southeast Asia strategies typically list the same initiatives: local-flavour limited editions, packaging in national languages, celebrity marketing campaigns, halal certification applied to existing product lines.

These are surface adaptations. They do not change the product’s price architecture, the cost base it was built on, or the distribution model it requires. Documented cases of genuine localisation look structurally different.

Yili in Indonesia

Chinese dairy brand Yili entered Indonesia’s ice cream market in 2018 and captured 5% of the local market by 2024, not by competing in modern retail, but by building a distribution model around Indonesia’s grocery-dominated channel, partnering with retailers to install freezers where Indonesian consumers actually shop.

That is a distribution decision, not a marketing decision. Yili did not adapt its packaging and enter the same channels Western brands default to. It redesigned its route to market around the 70% the modern retail model does not reach.

“We chose to become a Joyday distributor because of Yili’s reputation as a leading global company, its strong commitment to quality, and the large growth potential in the Indonesian market. Since we partnered in May 2018, we have expanded our distribution network, strengthened our operations team, and increased penetration across modern and traditional markets. We also continue to innovate in marketing strategies to ensure Joyday’s stable and sustainable growth locally.” — Levina Adrianne Tanza, Director of PT Panjunan

Mixue Bingcheng Southeast Asia expansion

Mixue Bingcheng’s Southeast Asia expansion produced 6,100-plus outlets across the region by 2025. Its pricing is competitive with street food, not with premium coffee. Its menu includes format-specific localisations: Gula Melaka in Malaysia.

It does not position as an affordable version of a Western product; it positions as an affordable local product with a scaled supply chain behind it. The distinction matters because it determines who the consumer is comparing the product against.

The Brands That Have Made It Work — and What They Have in Common

In 2025, brands such as Nestlé’s Milo, Nescafé, Unilever, and Ensure continue to hold strong positions across Southeast Asia. Their success demonstrates that Western brands can thrive in the region when they adapt to local market conditions.

What these brands have in common is a long-term commitment to localisation. They entered the market early, invested in local manufacturing, built broad distribution networks, and aligned their pricing with local consumer expectations. Milo, for example, is marketed as an affordable everyday beverage rather than a premium imported product.

Over time, these companies stopped operating like foreign brands in the decisions that matter the most, pricing, production, and distribution, and instead built business models around local market realities.

Three Diagnostic Questions for Any Western Brand Considering Southeast Asia Entry

For Western brand managers and market entry consultants evaluating Southeast Asia expansion, three diagnostic questions cut through the market-sizing optimism before a budget is committed.

1. Is your price point viable in Indonesia and Vietnam, not just Singapore?

Singapore’s premium retail environment is not representative of Southeast Asia. Test your pricing and margins against Indonesian and Vietnamese consumer expectations first.

2. How will you reach the 70% of sales that come from independent outlets?

Focusing only on modern retail chains and premium malls addresses a limited portion of the market. A clear strategy for independent retailers is essential from the start.

3. Does your localisation strategy go beyond branding?

Localisation strategy for F&B in Southeast Asia is not limited to local-language packaging and new flavours. Successful brands adapt pricing, sourcing, production, and distribution models to local market realities.

Key Takeaway: The most successful brands in Southeast Asia localise their entire business model, not just their marketing.

The Leading Indicator to Watch: Chinese Brand Expansion in 2026

Chinese brands are becoming an important test case for Southeast Asia expansion. Their success or failure in price-sensitive markets like Indonesia and Vietnam will help shape the Southeast Asian food trends playbook for future entrants.

If these brands can build profitable scale, Western companies can learn from their approach, or acquire brands that have already proven the model. If they struggle, it will show that success in Southeast Asia depends less on brand origin and more on pricing, margins, and distribution.

The key challenge is meeting middle-class food preferences in Asia, where consumers already have plenty of local and international choices competing for their attention.

Data Sources

Source |

Organization |

| Southeast Asia Foodservice Market Size & Share Analysis – Growth Trends and Forecast (2026–2031) | Mordor Intelligence |

| Independent Outlets Market Share in Southeast Asia | Mordor Intelligence (via MarketResearch.com) |

| ZUS Coffee vs Starbucks in Malaysia 2025 | GrowthHQ |

| Thailand’s Café Amazon Ramps Up Global Expansion via Franchising | QSR Media |

| FT Confidential Research Survey | Financial Times (FT Confidential Research) |

| Indonesia: Food Service – Hotel Restaurant Institutional Annual | U.S. Department of Agriculture (USDA Foreign Agricultural Service) |

| Chinese Food Brands Localising Products to Crack South East Asian Markets | FoodNavigator Asia |

| Make Room Starbucks and McDonald’s. China’s Mixue and Other Brands Win Fans in Southeast Asia | CityNews/The Associated Press (AP) |

| Yili Indonesia Expands Distributor Partnerships to Strengthen Joyday’s Market Reach and Support Sustainable Ice Cream Growth Nationwide | Jakarta Daily |