The Southeast Asia foodservice market is expected to reach USD 252.85 billion in 2026, reaching USD 465.45 billion by 2031 at a 12.98% CAGR.

The ASEAN food and beverage industry in 2026 is, by any measure, in a high-growth phase. International visitor arrivals nearly doubled between 2022 and 2023. A young, urbanising population across a 680-million-person region is dining out more frequently. The macro story is a growth investor’s dream.

That headline number is real. It is also dangerously incomplete. Most coverage of Southeast Asia’s F&B growth reads the macro and stops there.

This piece reads the structural conditions underneath. The five risks below are not predictions. They are conditions that are already present and already affecting operators who entered without accounting for them.

Revenue growth in local currency does not mean margin safety at the operator level. And the gap between those two numbers is where the real story lives.

Five Structural Risks that Operators and Investors are Not Pricing in

These five risks share three characteristics: each is structural (not temporary), already observable (not speculative), and specific to Southeast Asia (not generic global risk). They are not reasons to avoid the market; they are conditions to price in correctly.

Risk 1 – Supply Chain Fragility Masked by Short-term Stability

The claim to defend: Southeast Asia’s F&B supply chains are more concentrated and more single-sourced than operators typically acknowledge. The post-pandemic period created an illusion of recovery: imports resumed, logistics normalised, costs stabilised. But the underlying structural fragility was not fixed; it was masked.

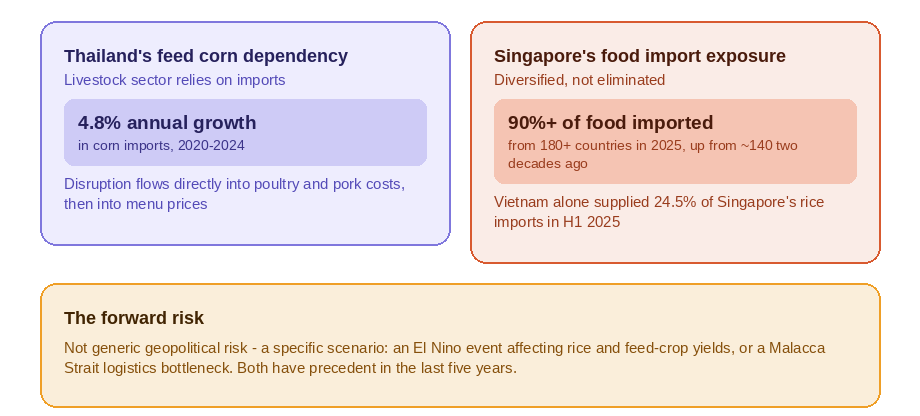

Take Thailand. The country’s livestock sector relies on imported corn to meet rising feed demand, Thailand’s corn imports grew at an average of 4.8% annually between 2020 and 2024. Any disruption to that supply chain, a climate event, a trade restriction, a logistics bottleneck, flows directly into poultry and pork costs, then into menu prices.

Singapore’s exposure is even more acute. The city-state imports more than 90% of its food. In 2025, it sourced from over 180 countries, up from about 140 two decades ago, but that diversification is a risk-reduction strategy, not a risk-elimination one.

That said, a high proportion of Singapore’s rice, vegetables, fruit and seafood still comes from a concentrated set of Southeast Asian sources. Vietnam alone supplied 24.5% of Singapore’s rice imports in the first half of 2025.

“At the moment we haven’t increased prices, but we are coming to a point where we cannot keep absorbing this cost increase because the fuel cost is not a small jump, it’s a big one.” said Mr Malcolm Ong, founder of The Fish Farmer.

The forward risk: The next plausible disruption is not generic “geopolitical risk.” It is a specific scenario: an El Niño event affecting rice and feed-crop yields across the region, or a South China Sea logistics bottleneck that concentrates shipping delays through the Malacca Strait. Neither is hypothetical; both have precedent in the last five years.

Risk 2 – Labour Shortages are Structural, Not Cyclical

The F&B labour shortage in Southeast Asia is consistently framed as a post-pandemic recovery problem. It is not. The pipeline of trained culinary and FOH talent was already thinning before 2020.

The data is stark. In Vietnam, 88% of F&B businesses reported being critically short-staffed. Driven by high turnover and a lack of skilled applicants, chains aggressively hired frontline workers, with bartending demand jumping 62% and kitchen assistant requests rising 33%.

Malaysia tells a similar story. The F&B sector has one of the highest turnover rates. The sector’s labour shortage stems from perceived job insecurity, foreign worker recruitment restrictions, and changing work expectations among young Malaysians.

Retail, F&B and hospitality are among Malaysia’s largest youth employers, but also the most strained by high turnover, staffing shortages and tight margins.

The pre-COVID trend is unmistakable. Singapore’s Shatec, a hospitality training institution that had operated for over four decades and graduated approximately 40,000 individuals, began winding down operations in April 2025. The school’s main campus building was put up for sale. It is a structural contraction in the very institutions that were supposed to supply the industry’s future talent.

The structural fix attempt: Singapore has recognised the problem. The Singapore Tourism Board points to continuing education providers such as Republic Polytechnic, Temasek Polytechnic, and various Workforce Skills Qualifications-accredited training organisations.

Some have called for the creation of a National Culinary and Hospitality Institute. But these are long-lead solutions to a problem that is already constraining growth.

Risk 3 – Regulatory Divergence Across ASEAN is a Hidden Expansion Cost

Many companies assume that if their products meet the regulations in Singapore or Malaysia, they can easily sell them across the rest of Southeast Asia. In reality, ASEAN is made up of 10 countries, and each has its own food regulations, import rules, labelling requirements, and certification processes.

Regulatory differences remain one of the biggest barriers to regional trade. Countries such as Singapore, Malaysia, and Vietnam are more closely aligned with international food standards, while Indonesia and Thailand have only partial alignment.

“Many MSMEs have found the halal certification process undertaken by larger companies to be too complicated and too costly, leading to many challenges in the transition of this group to complete their certifications.” Indonesia Halal Product Assurance Agency (BPJPH) Department of Halal Registration and Certifications Head Dr Mamat Salamet Buranudin.

Cambodia, Laos, and Myanmar are still developing many of their regulatory systems. As a result, businesses often need to meet different requirements in every emerging food market.

Similarly, customs clearance can take just a few hours in Singapore but several days in other ASEAN markets. Cold-chain infrastructure is another challenge, with only a small percentage of perishable goods being transported through temperature-controlled logistics across the region.

The priority: A product or format that clears regulatory requirements in one market may require full reformulation, relabelling, or a different ownership structure in the next. Budget for country-specific regulatory work in each market before the expansion timeline, not after the product is developed.

Risk 4 – Faster than Revenue Growth

The claim to defend: Revenue growth in local currency can be margin erosion in USD. Most F&B input costs in Southeast Asia are import-priced in USD or hard currency, while revenue is collected in local currency.

Thailand’s baht appreciated from 34.1 to 32.7 against the USD by 30 June 2025, gaining 10.4% against the dollar over the course of the year to become Asia’s second-best performing currency. A stronger baht hurts exports, as Thai rice exports fell 25.1% year-on-year in the first seven months of 2025, but it is a double-edged sword for importers. A weaker baht, conversely, raises the cost of imports, from energy and food products to electronics and automobiles.

Indonesia’s rupiah has been even more volatile. The rupiah closed at Rp 17,995 per US dollar this jun 2026, down 43 points from Rp 17,950 in the previous session. Therefore, when the rupiah depreciates beyond Rp16,700/USD, import costs automatically increase.

Vietnam maintained an increase of about 3–3.5% against the USD in 2025. Logistics costs, freight rates, and marine insurance remained high due to global trade and geopolitical instability.

The import dependency problem: For a hotel or restaurant operator in Bangkok, that means 30–35% of your cost base is exposed to USD-denominated price movements, and you collect revenue in baht. When the baht weakens, margins compress immediately. Menu price increases can offset some of the impact, but only up to the point of demand destruction.

Also, there is a limitation. Currency hedging is not accessible to most independent operators or even mid-size restaurant groups. This is a structural disadvantage vs. large multinationals.

For the independent restaurateur opening in Bangkok or Jakarta, currency risk is an unhedged P&L exposure that can swing margins by several percentage points in a single quarter.

Risk 5 – Consumer Premiumisation is Uneven, and the Middle is Disappearing

The Southeast Asia F&B premiumisation narrative is accurate at the top of the market and misleading in the middle. High-net-worth and upper-middle consumer food trends in Jakarta, Bangkok, Ho Chi Minh City, and Singapore reflect that they are spending more on dining experiences.

But the mass-market middle, the consumer segment that sustains mid-scale restaurant and QSR formats, is under pressure.

Thailand’s restaurant sector is facing what one observer called a “boiling frog” crisis. Around 3,000 restaurants closed during the first quarter of 2025. The segments showing strong performance include mass-market restaurants and QSR formats. The middle is where the pressure is concentrated.

Also, a new wave of expansion by global and Chinese food brands is reshaping the QSR landscape across Southeast Asia, forcing local players to adopt technology and rethink customer strategies to survive. Frequent pricing swings strain loyalty as consumers tire of ongoing market changes.

Lastly, the gap between real wage growth and food inflation is the margin squeeze on the mid-market consumer. In Malaysia, hospitality sector wage growth decelerated in 2025. Meanwhile, food inflation has been persistent.

The consumer in the middle, the one who sustains mid-scale restaurant formats, is feeling the squeeze from both sides: higher food prices and stagnant real wage growth. Thus, operators who built their format for the middle are finding that the middle is not growing as fast as the headline consumer confidence numbers suggest.

The Counter-Argument: The Case for Optimism

The long-term fundamentals are genuinely strong. A young, urbanising, increasingly affluent population across the region. Rising dining-out frequency. Significant underpenetration of modern F&B formats in tier-2 and tier-3 cities.

Growing inbound tourism. Major hotel groups are expanding. Private equity is allocating. These are not signals of a market about to contract. The Southeast Asia F&B market, foodservice category is projected to grow at nearly 12.98% CAGR through 2031. That is not a market in trouble; that is a market with genuine tailwinds.

How to answer it: All of that is true, and none of it means the risks above do not apply. The operators who are succeeding in Southeast Asia are succeeding because they understood the structural conditions before they entered, not because the tailwinds were strong enough to overcome bad planning.

Macro optimism and risk-adjusted entry strategy are not in conflict. This piece is making the second argument, not disputing the first.

The Implication: What this Means for F&B Operators Planning Market Entry in 2026

The cost of expanding into Southeast Asia goes well beyond rent, staffing, and marketing. Operators need to account for supply chain risks, labour constraints, and country-specific regulations before entering a new market.

Building these factors into expansion plans early helps avoid unexpected costs, delays, and pressure on profitability.

Audit your supply chain before market entry

Map your import dependency by ingredient category before signing a lease. Identify which ingredients have no local substitute and model the impact of a potential increase in import costs.

Build your financial model around realistic labour costs

Base forecasts on local turnover rates, recruitment costs, and ongoing training-not on the assumption that labour costs will mirror your home market. F&B businesses in Vietnam report being short-staffed, making labour shortages a structural challenge rather than a temporary one.

Treat compliance as a market-specific investment

Do not assume regulatory approval in one ASEAN country will transfer to another. Budget for country-specific compliance work before product development and expansion. Indonesia’s mandatory halal certification deadline on 17 October 2026 is one example of how local regulations can directly affect market entry timelines.

The Forward Look: What to Watch in the Next 12 Months

Three signals will tell us whether the risks above are being priced in – or still being ignored.

First, watch Indonesia’s Q3–Q4 2026 consumer confidence data. If mid-market F&B spending shows recovery, the premiumisation split may be narrowing. If it continues to lag premium spending, the middle-market squeeze is structural.

Second, watch Singapore’s MAS monetary policy and SGD trajectory in H2 2026. As the region’s pricing benchmark, SGD strength or weakness affects import costs across Southeast Asian F&B supply chains. A weaker SGD raises import costs for the entire region.

Third, watch the FHA 2027 exhibitor mix. If the proportion of local Southeast Asian suppliers increases year-on-year, the supply chain innovation and localisation trend is real.

If the exhibitor floor is still dominated by international suppliers, the import dependency risk has not moved. FHA is the primary data source for what brands are betting on, and the exhibitor mix at FHA 2027 will be the clearest signal of whether operators are actually localising, or just talking about it.

Data Sources

| Source | Data used |

| Asian Agribiz – Thailand tightens the belt on feed corn imports to drive green sourcing | Thailand’s tighter import controls on agricultural commodities, highlighting evolving sourcing policies and supply chain risks. |

| Singapore Food Agency – Singapore continues to strengthen its food supply resilience | Singapore’s reliance on food imports, diversification strategy, and national food resilience initiatives. |

| Mordor Intelligence – Southeast Asia Foodservice Market | Southeast Asia foodservice market size, growth forecasts, industry trends, and import dependency insights. |

| KPMG Thailand – Capital Market and Business Valuation Insights Issue 009 | Economic outlook, inflation, consumer spending, and business environment affecting F&B operators in Thailand. |

| Jakarta Globe – Rupiah nears Rp18,000 as weak PMI, reserve concerns weigh | Indonesian currency volatility and its implications for imported food costs and operating expenses. |

| The Nation Thailand – Trade news | Thailand’s trade and import developments relevant to food sourcing and supply chain planning. |

| MarketResearch.com – Southeast Asia Foodservice Market Report (Mordor Intelligence) | Additional market data supporting foodservice growth projections, competitive landscape, and regional trends. |

| The Straits Times – Less than 1% of food in Singapore comes from the Middle East, but food prices could still go up | Impact of global geopolitical events on Singapore’s food prices despite diversified import sources. |